All Categories

Featured

Table of Contents

- – Is there a budget-friendly Guaranteed Interest...

- – What types of Indexed Universal Life Investmen...

- – What is Guaranteed Iul?

- – Indexed Universal Life Premium Options

- – What happens if I don’t have Iul Policy?

- – Why should I have Long-term Iul Benefits?

- – Is there a budget-friendly Indexed Universal...

In case of a lapse, impressive policy car loans in unwanted of unrecovered expense basis will go through regular earnings tax obligation. If a plan is a modified endowment contract (MEC), plan lendings and withdrawals will be taxable as average revenue to the level there are earnings in the policy.

It's essential to keep in mind that with an exterior index, your plan does not straight get involved in any kind of equity or fixed revenue investments you are not purchasing shares in an index. The indexes offered within the policy are created to maintain track of diverse sections of the U.S

Is there a budget-friendly Guaranteed Interest Iul option?

An index may influence your rate of interest credited, you can not get, straight participate in or get dividend settlements from any of them with the policy Although an external market index might impact your rate of interest credited, your plan does not directly take part in any stock or equity or bond investments. IUL accumulation.

This material does not use in the state of New york city. Guarantees are backed by the financial toughness and claims-paying capacity of Allianz Life insurance policy Company of The United States And Canada. Products are provided by Allianz Life insurance policy Business of The United States And Canada, 5701 Golden Hills Drive, Minneapolis, MN 55416-1297. .

Safeguard your liked ones and conserve for retired life at the same time with Indexed Universal Life Insurance Policy. (Indexed Universal Life)

What types of Indexed Universal Life Investment are available?

HNW index global life insurance can help gather money worth on a tax-deferred basis, which can be accessed throughout retired life to supplement revenue. (17%): Insurance holders can typically borrow versus the cash money worth of their policy. This can be a resource of funds for different demands, such as investing in a service or covering unforeseen expenses.

The death advantage can help cover the prices of searching for and training a substitute. (12%): Sometimes, the cash money worth and survivor benefit of these policies may be safeguarded from financial institutions. This can give an extra layer of economic protection. Life insurance policy can also aid reduce the danger of a financial investment portfolio.

What is Guaranteed Iul?

(11%): These plans use the prospective to earn rate of interest linked to the efficiency of a stock exchange index, while likewise providing an ensured minimum return (Guaranteed IUL). This can be an eye-catching option for those seeking growth capacity with drawback defense. Resources forever Research Study 30th September 2024 IUL Study 271 respondents over thirty day Indexed Universal Life insurance policy (IUL) might seem complex initially, yet recognizing its auto mechanics is essential to comprehending its complete possibility for your monetary preparation

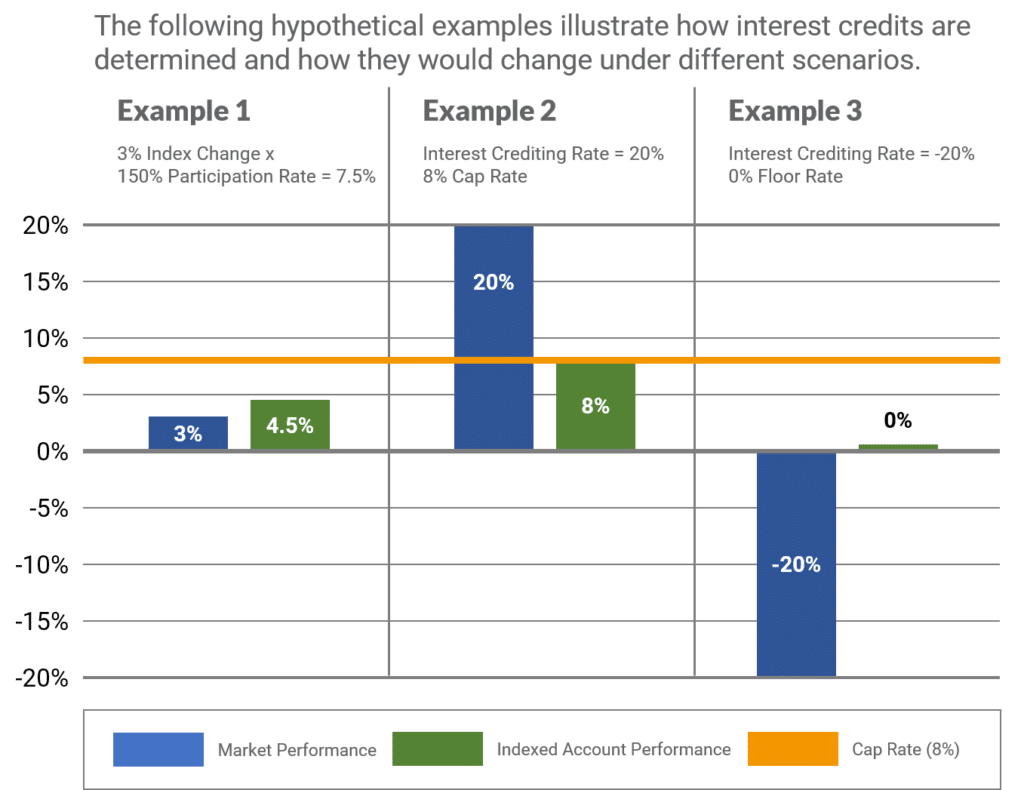

As an example, if the index gains 11% and your participation price is 100%, your cash value would certainly be attributed with 11% passion. It is essential to keep in mind that the maximum interest attributed in a given year is topped. Allow's say your picked index for your IUL plan gained 6% initially of June to the end of June.

The resulting interest is included to the cash value. Some plans calculate the index obtains as the amount of the adjustments for the duration, while other policies take an average of the everyday gains for a month. No passion is attributed to the cash money account if the index goes down as opposed to up.

Indexed Universal Life Premium Options

The rate is set by the insurance coverage business and can be anywhere from 25% to more than 100%. IUL plans usually have a floor, often established at 0%, which shields your cash money value from losses if the market index does adversely.

This gives a degree of security and satisfaction for insurance holders. The rate of interest credited to your cash worth is based upon the performance of the chosen market index. A cap (e.g., 10-12%) is usually on the optimum rate of interest you can gain in a provided year. The part of the index's return credited to your money value is identified by the participation rate, which can vary and be adjusted by the insurance firm.

Store about and compare quotes from various insurance coverage companies to discover the finest plan for your needs. Prior to picking this type of policy, guarantee you're comfortable with the potential changes in your cash money worth.

What happens if I don’t have Iul Policy?

By contrast, IUL's market-linked money value growth supplies the capacity for higher returns, particularly in beneficial market conditions. This capacity comes with the risk that the supply market efficiency might not deliver regularly steady returns. IUL's adaptable costs repayments and adjustable death advantages supply flexibility, appealing to those looking for a plan that can develop with their changing monetary scenarios.

Indexed Universal Life Insurance Coverage (IUL) and Term Life insurance policy are various life plans. Term Life insurance policy covers a certain period, generally in between 5 and 50 years. It only gives a fatality benefit if the life insured passes away within that time. A term policy has no cash money value, so it can not be used to provide lifetime advantages.

:max_bytes(150000):strip_icc()/dotdash-ask-answers-205-Final-7a1ca51b85d44e0d81dc7b46f919180d.jpg)

It appropriates for those seeking short-term defense to cover details financial commitments like a home loan or youngsters's education costs or for business cover like shareholder security. Indexed Universal Life (IUL), on the other hand, is a long-term life insurance policy that offers protection for your entire life. It is extra pricey than a Term Life policy due to the fact that it is designed to last all your life and provide an assured money payout on fatality.

Why should I have Long-term Iul Benefits?

Picking the best Indexed Universal Life (IUL) policy is concerning locating one that lines up with your financial goals and risk tolerance. A knowledgeable monetary advisor can be invaluable in this process, assisting you through the complexities and ensuring your picked policy is the best suitable for you. As you investigate acquiring an IUL policy, keep these vital factors to consider in mind: Comprehend how credited rates of interest are linked to market index efficiency.

As outlined earlier, IUL policies have different fees. Understand these prices. This identifies just how much of the index's gains add to your money worth growth. A higher price can boost possible, however when comparing plans, assess the cash value column, which will assist you see whether a higher cap rate is much better.

Is there a budget-friendly Indexed Universal Life For Retirement Income option?

Study the insurance firm's monetary rankings from agencies like A.M. Best, Moody's, and Standard & Poor's. Various insurance companies provide variants of IUL. Job with your consultant to comprehend and locate the most effective fit. The indices connected to your plan will directly affect its performance. Does the insurance company offer a range of indices that you want to align with your investment and danger profile? Flexibility is essential, and your policy must adjust.

{kind=link}

Table of Contents

- – Is there a budget-friendly Guaranteed Interest...

- – What types of Indexed Universal Life Investmen...

- – What is Guaranteed Iul?

- – Indexed Universal Life Premium Options

- – What happens if I don’t have Iul Policy?

- – Why should I have Long-term Iul Benefits?

- – Is there a budget-friendly Indexed Universal...

Latest Posts

Iul Dortmund

Universal Underwriters Life Insurance

Best Iul Insurance Companies

More

Latest Posts

Iul Dortmund

Universal Underwriters Life Insurance

Best Iul Insurance Companies